![Bit com]()

![]()

![]()

![]()

![MusicLM]() MusicLM

MusicLM

![3D Parallax Background]() 3D Parallax Background

3D Parallax Background

![Custom Skin Creator]() Custom Skin Creator

Custom Skin Creator

![Al Ansari]() Al Ansari

Al Ansari

![Avast Battery Saver]() Avast Battery Saver

Avast Battery Saver

![Easy Setup Assistant]() Easy Setup Assistant

Easy Setup Assistant

![HitmanPro]() HitmanPro

HitmanPro

![Yumy]() Yumy

Yumy

Bit com

0

Download

Category: Services

System: Android 5.0

Program Status: Free

Looking at the file: 52

Description

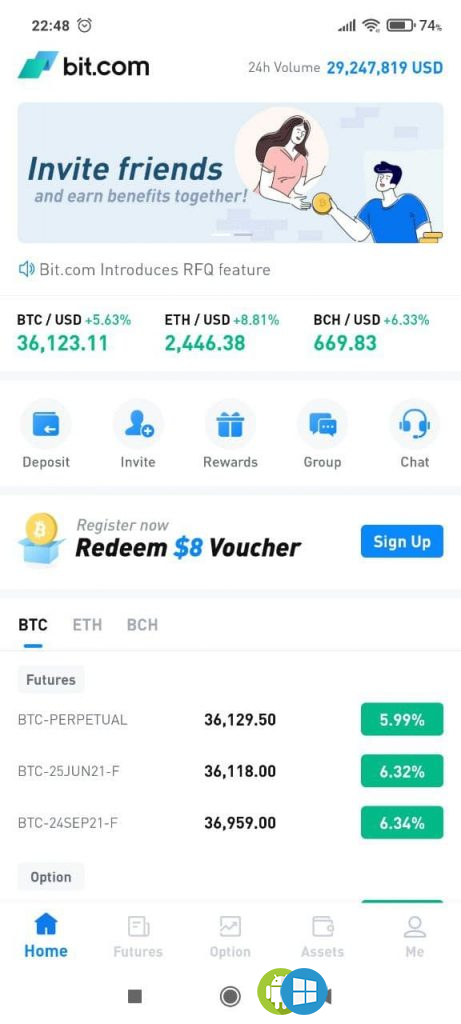

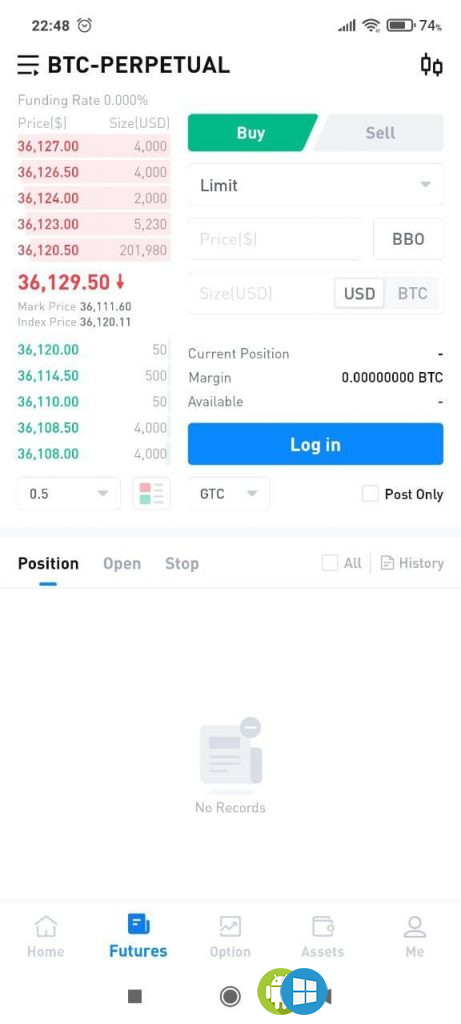

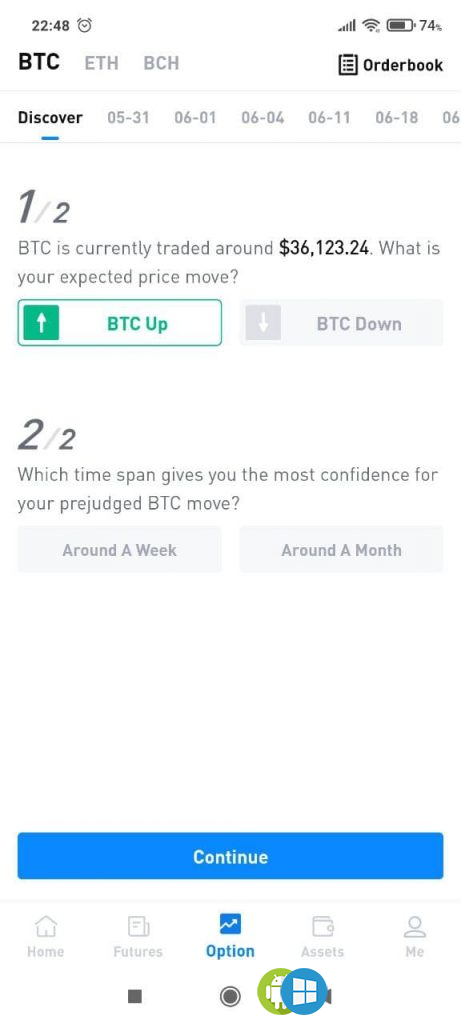

Bit com is a free utility through which people can access a well-known exchange specializing in trading electronic currencies. It is possible to sell, exchange and buy different coins, including Ethereum and Bitcoin Cash. In addition to this, it is possible to trade binary options and futures.

Trading

The software acts as a mobile client of a popular platform, on which a variety of assets are traded. Among other things, participants of the online service are able to buy, exchange and sell electronic currencies. Namely: Bitcoin Cash, Ethereum and Bitcoin. In addition, the online platform provides a platform for trading options and futures.Service functionality

The creators of the platform added the ability to track the price dynamics of the currencies available for trading. In addition, the user is able to study the total trading volume for the last day. Such information can be useful when deciding whether to buy or sell an electronic asset. The mobile utility has access to the archive of past trading operations, stock exchange stack and other useful functions for traders. The trading process itself is extremely simple, which allows you to quickly make various transactions.Platform security

The developers of the online service claim a high degree of protection for all transactions passing through the exchange, as well as information about user wallets. To ensure full-fledged data security, the platform uses advanced technologies. If for some reason the service participants still lose their assets, the creators promise to compensate them from a special fund.Features

- Online trading platform;

- Full support for many versions of OC;

- There are trades in electronic currencies, futures and other;

- Reliable security system.

Screenshots

Download Bit com

See also:

MusicLM is an Android application that provides access to a music track creation service using a...

3D Parallax Background

3D Parallax Background

3D Parallax Background is a free tool, it allows all users to set unique desktops that are...

Custom Skin Creator is an Android application for generating and using custom textures for...

Al Ansari is the official Android client of a major stock exchange company based in the UAE. You...

Avast Battery Saver is a software tool from the developers of the popular antivirus. Through this...

The Easy Setup Assistant application is designed for quick setup of TP-LINK routers. It requires a...

HitmanPro is a specialized software that can quickly scan a computer machine for viruses. It...

Yumy is an online service that can be used on Android gadgets. With the help of the utility, users...

Comments (0)